Regulatory greenfield

How the CFTC went from blocking prediction markets to rolling out the red carpet

The United States had all of fifteen active futures exchanges in 2019. That was the low point of a decades-long consolidation that had compressed the industry into a duopoly of CME Group and ICE, with a handful of niche survivors on the margins.

As of early 2026, there are twenty-six, with a dozen more applications officially pending1.

Seven new Designated Contract Markets were approved in 2025 alone. The forthcoming pipeline reads less like a regulatory docket and more like a venture portfolio: Sporttrade, Juice Exchange, Water Street Labs, Optex Markets, Ludlow Exchange. The most recent approval, Xchange Alpha, came through in 204 days, the fastest ever, close to the statutory minimum of 180 days. The industry hasn’t seen this pace of expansion since the regional grain exchange era of the late 1800s.

Something structural has changed. The prediction market exchange business, which for most of its history required Fortune 500-scale resources and years of regulatory patience, is becoming accessible to well-funded startups. The barriers are falling from multiple directions at once: a new CFTC chairman with an explicitly permissive posture, a collapsing cost curve for acquiring the necessary licenses, and a pending regulatory framework that could streamline the process further still.

The chairman’s signal

The expansion didn’t happen by accident. It has a political catalyst, and his name is Michael Selig.

Selig was confirmed as CFTC chairman on December 18, 2025, and currently serves as the commission’s sole member. No other commissioners have been confirmed. What the chairman wants, the chairman gets.

What Selig wants became clear on January 29, 2026, when he made his first public remarks at a joint CFTC-SEC summit and laid out a four-part agenda for event contracts: withdraw the proposed rule that would have banned sports and political event contracts, rescind the 2025 staff advisory warning exchanges to prepare for state-level prohibitions, direct staff to draft new affirmative rules, and reassess the CFTC’s participation in pending federal litigation to defend its exclusive jurisdiction over commodity derivatives. He called for the “minimum effective dose of regulation” and announced the “Future-Proof“ initiative, a comprehensive review of existing rules to modernize them for new entrants.

The contrast with his predecessors is sharp. Under Chairman Rostin Behnam, the CFTC fought Kalshi in federal court over whether political event contracts were permissible, and a proposed rule would have prohibited sports and political event contracts outright. Selig reversed all of it within weeks of taking office.

But the formal actions only tell half the story. On February 5, when Chris Christie tweeted that prediction markets are violating the law, Selig quote-tweeted him with two words: “Strong Disagree.” Two days later, when a reporter quoted AOC calling the rise of prediction markets “bad,” Selig responded: “CFTC officially back on track.”

The chairman of a federal regulatory agency is treating political opposition to the industry he oversees as confirmation that he is doing his job correctly. That is not how agency heads normally behave. For anyone considering filing a DCM application, the signal could not be louder.

Even just yesterday, Selig went further still, publishing an op-ed in the Wall Street Journal announcing that the CFTC would file an amicus brief supporting Crypto.com against state regulators in the Ninth Circuit, calling state litigation an attempt to 'undermine the agency's exclusive jurisdiction. You can read more about that legal fight here:

A collapsing cost curve

To operate a prediction market exchange in the United States, you have historically needed up to three separate federal registrations: a Designated Contract Market (DCM), a Derivatives Clearing Organization (DCO), and either your own Futures Commission Merchant (FCM) or a relationship with one. Each carries its own application process, compliance infrastructure, and capital requirements. The DCM alone requires financial resources equal to at least twelve months of projected operating expenses. You need the business substantially built before you even file.

Three things are changing, and together they’ve turned what used to be a Fortune 500-scale undertaking into something a well-capitalized startup can credibly attempt.

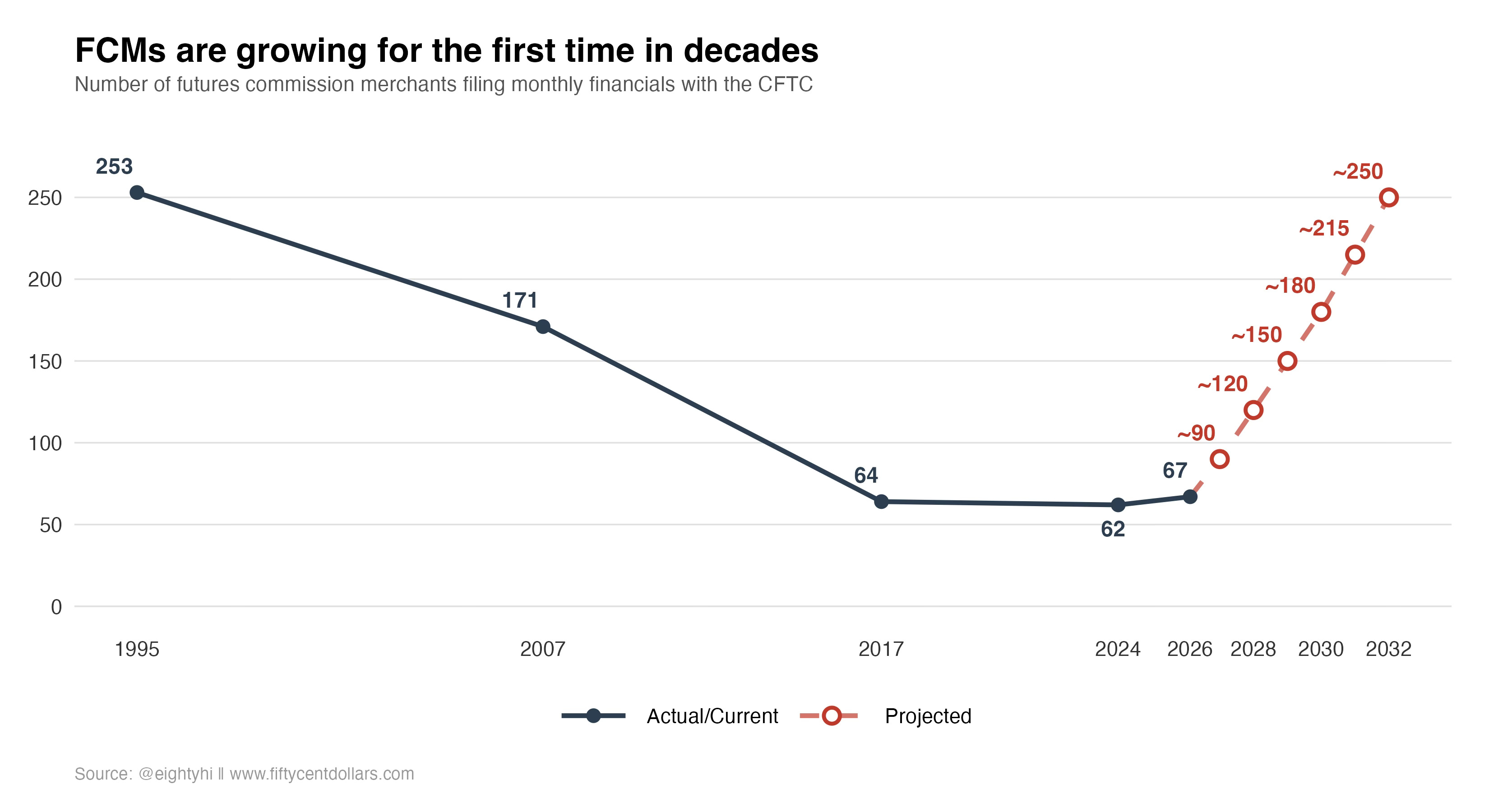

First, the regulated distribution layer has blown wide open. A year ago, the only way an American consumer could legally trade prediction markets was through Kalshi / Crypto.com directly, or through Robinhood. Now there are at least a dozen entry points, and the pace of new approvals is accelerating. For three decades, the number of registered FCMs in the United States did nothing but shrink, from 253 in 1995 to 62 in 20232. The prediction market wave has pushed that number back to 67.

PrizePicks became the first fantasy operator to receive FCM status from the NFA in September 2025. DraftKings got approved as an introducing broker in December and launched DraftKings Predictions before the month was out. Fanatics skipped the application process entirely by acquiring Paragon Global Markets, an already-approved IB, and had Fanatics Markets live in 24 states within weeks. Underdog and Sleeper both received FCM approval in January 2026.

The CFTC acknowledged the shift in June 2025, publishing an FCM FAQ in response to what it described as an ‘increased number of inquiries’ from new entrants drawn to event contracts.

There’s an even lighter-weight path: before getting its FCM, Underdog launched sports contracts in 16 states as a technology service provider to Crypto.com’s DCM, bypassing NFA registration altogether (though at the cost of co-branding and ceding customer ownership to the exchange).

Second, the exchange layer itself is getting cheaper. Time is the real cost for a pre-revenue startup, and the CFTC’s approval clock has historically run far longer than the 180-day statutory review period.

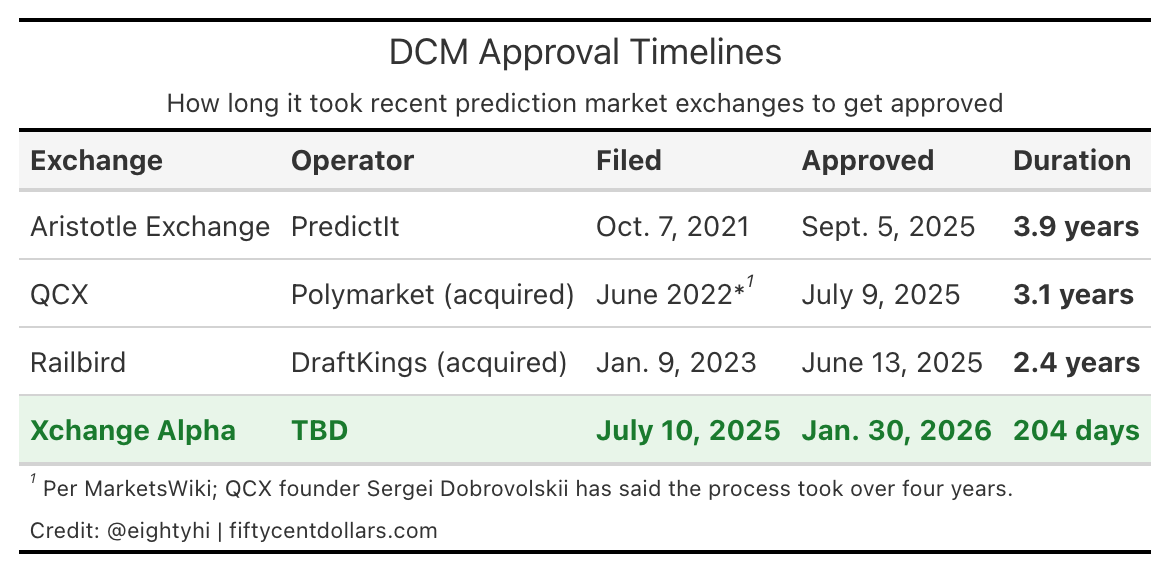

The table tells a clear story. Aristotle, QCX, and Railbird each waited between two and four years. Xchange Alpha submitted its application on July 10, 2025 and received its designation on January 30, 2026: 204 days, essentially at the statutory pace, the fastest ever.

One data point does not make a trend. But former acting chair Caroline Pham congratulated Xchange Alpha’s chief legal officer on LinkedIn and wrote, “Another approval in approximately 7 months,” suggesting the compression started under her tenure. If the Selig CFTC maintains that pace, the effective cost of entry drops by an order of magnitude in pre-revenue burn alone.

“We just processed, I think in a record time of two hundred days one of the more recent exchange applications”

Chairman Selig on a recent episode of Odd Lots.

Third, the CFTC is actively considering whether to streamline the clearing layer. Kalshi proved you don’t need the full three-license stack: it operates as both a DCM and DCO under one corporate group, onboarding retail customers directly without an FCM in the loop. That’s a unique anti-pattern for derivatives exchanges. Neither CME nor ICE nor CBOE have ever had a consumer-facing app that directly onboards “self-clearing” exchange members.

But now, a December 2025 Request for Comment issued by the CFTC asked whether a separate registration sub-category should be created for retail-oriented (see: fully collateralized with no leverage) clearing organizations. The direction of travel is clear: the Commission is working to fit the regulatory architecture to the product, rather than forcing prediction markets into a framework designed for agricultural futures in the 1970s.3

The combined result is that every layer of the regulatory stack is getting thinner. The distance between “we have an idea” and “we’re taking our first trade” has shortened from years to potentially months.

It’s kind of like how SpaceX made it cheaper to launch satellites, and now there’s going to be tons of satellites. We may see a huge proliferation of the market structure in this industry.

What comes next

If the current trajectory holds, the number of active DCMs will almost certainly surpass 40 by the end of 2027. The United States is about to have more futures exchanges than at any point since the Great Depression.

Most of the new entrants are chasing sports event contracts, where the proven revenue sits. A few crypto derivatives play positioning for the Digital Asset Market Structure Act. Some are building toward novel categories. And at least a handful of the pending DCM licenses will likely be acquired before they ever list a contract, bought by distribution platforms that already have the customer base but lack the regulatory charter.

This is the part of the cycle that’s easy to forecast. What’s harder is what happens after the proliferation. Every wave of barrier reduction in American exchange history resulting in proliferation has been followed by consolidation. Whether prediction markets will follow that pattern is the most important structural question in the industry.

There are reasons to think this time is different: the products are heterogeneous rather than fungible, the markets are retail-native rather than institutional so the network effect of liquidity isn’t as strong, and the startup costs that cemented the CME’s dominance are falling.

The market structure question deserves its own treatment4. For now, the facts on the ground are clear enough. The regulatory barriers that defined this industry for decades are falling, the chairman of the CFTC is publicly cheering the process along, and the pipeline of new entrants suggests the market believes him.

Pending DCM applications on the CFTC portal as of February 2026 include Sporttrade (the sports betting exchange pivoting to federal regulation), Juice Exchange, Water Street Labs, Ludlow Exchange (affiliated with sweepstakes sportsbook Novig), Optex Markets, XV Exchange (affiliated with Canadian sports exchange STX), tZERO DCM (the digital assets firm), ProphetX, RSBIX, OneChronos Markets, and PMEX Markets (an AI compute derivatives play). Several additional legacy applications from 2013-2016 also remain technically pending.

This is also illusory, there are likely many, many more getting ready to submit their applications.

Sources:

1995: 253 FCMs Emm, E., Gay, G., Ma, C., & Ren, H. (2019). “Futures commission merchants, customer funds and capital requirements.” Journal of Futures Markets, 39(9), 1055-1075. doi.org/10.1002/fut.22020

2007: 171 FCMs (March) Peirce, H. (2017). “Dwindling numbers in the financial industry.” Brookings Institution, Center on Regulation and Markets, May 15, 2017, citing CFTC monthly financial data reports. brookings.edu/articles/dwindling-numbers-in-the-financial-industry

2017: 64 FCMs (March) Peirce, H. (2017). Same source as above.

2024: 62 FCMs CFTC FY2025 President’s Budget & Performance Estimate, Market Participants Division, March 2024. cftc.gov/sites/default/files/2024-03/FY2025BudgetRequest.pdf

2026: 67 FCMs (January) Author’s count from NFA membership records (nfa.futures.org/basicnet), incorporating 2025-2026 prediction market entrants (PrizePicks, Underdog, Sleeper, et al.).

The comment period on Release 9158-25 closed in February 2026, and the responses reveal genuine tension over how far simplification should go. Interactive Brokers, which operates ForecastEx, argued for "functional equivalence" in customer protections regardless of whether a customer accesses a market through an FCM or directly. An individual commenter flagged the AML blind spot created when you bypass the FCM entirely: DCOs aren't covered financial institutions under the Bank Secrecy Act, don't file Suspicious Activity Reports, and aren't examined for money laundering compliance. Better Markets opposed the entire concept, invoking FTX's failed direct-clearing proposal. These are real concerns about calibration. But they are concerns about the terms of simplification, not its direction.

You should subscribe if you haven’t 😉